|

Preparing vegetables will always demand some extra time and care. However, these days we're all trying to get more vegetables into our daily lives. Knowing more general ways to cook them only works in our favor. The transformation from raw to cooked never ceases to inspire and once you learn the overall cooking processes, you can tackle any vegetable like a pro. Below is just a start of ways you can experiment with vegetables but hopefully this inspire more vegetable cooking in your kitchen. BlanchingBlanching is a quick cooking process that involves submerging vegetables in boiling water for a short period of time. This process helps vegetables lose that extreme crispy bite that might be too much for some meals. Blanching works great for items like asparagus, broccoli and cauliflower but can also be great for greens. How to blanchTo blanch, bring a pot of salted water to a boil with a bowl of ice water nearby. Drop in your prepped vegetables and let them cook for only a few minutes. The timing will depend on the heartiness of what you're cooking. Spinach will take around 30 seconds while broccoli could be minutes. You want them to still be bright, colorful, and crisp but not crunchy. Strain the vegetables and transfer to the ice bath. How to use blanched vegetablesI like to use blanched vegetables for vegetable cakes, stir fries, or if I plan on pan-frying the vegetables after blanching. Getting blanching under your fingers is also a good thing to have in your pocket if you ever plan on freezing vegetables (which helps seal in color, flavor, and nutrients.) Example uses blanched vegetables:Broccoli Melts

RoastingOne of my favorite ways to cook harder vegetables like squash is by tossing them in oil and salt and popping them in a 425˚F oven. Let them roast under high heat for 30, 40, 50 minutes - I never really set a timer I just check them occasionally with a fork to test for softness and some good coloring. How to use roasted vegetablesRoasting vegetables is a great way to lock in flavor and have a bit of char-flavor to the items. Roasted vegetables are perfect as a side but I love adding them to all kinds of meals including pizza toppings, tacos, pasta, and salads. Example uses roasted vegetables:Sweet Chili Roasted Sweet Potato Spring Rolls

SteamingI often times forget about this option when I am preparing vegetables. When I think about cooking a sweet potato or a hard winter squash, I sometimes get mentally cornered into thinking that turning on the oven is the only way to get the job done. Steaming takes a fraction of the time, and is easier to clean up because there is no greasy oil or crusty bit of veg stuck to the pan. I highly recommend picking up a steaming basket. This makes steaming a bit easier because you can lift the vegetables out at the end of steaming. How to steam vegetablesFor steaming, all the vegetables should be roughly the same size, to cook evenly. Place about 1” of water in the bottom of a pot. This water should not touch the steaming basket, though. Bring that water to a boil, add your vegetables, turn the heat to a simmer, cover, and cook until the vegetables are just-tender. The vegetables should be bright in color still (similar to blanching). Remove the steaming basket and run the vegetables until cold water to stop the cooking process then season as desired! Steamed vegetables do well when finished with fats like olive oil, homemade aioli, or other types of rich sauces. How to use steamed vegetablesSteamed vegetables make for great side dishes. I also like to use steaming if I plan on pureeing something into a sauce or soup. You could also use as a filling for enchiladas, frittatas, or grain bowls. Example uses steamed vegetables:Carrot Baked Barley Risotto (calls for roasting but could use steamed carrots)

SautéingI used to be intimidated by the term sauté - I thought you were only doing it right if you managed to toss the food from your pan up into the air and back into the pan again with a graceful yet incredibly strong wrist action (luckily that's not so). How to sauté vegetablesSauté simply means to fry something quickly in a little hot fat. Cut your vegetables into evenly sized pieces, heat a pan with some oil or ghee, and toss in the vegetables. Coat them in the hot fat, and let the magic of fat and heat work wonders. Shoot for even coloring and frequent stirring until everything is tender and ideally caramelized or tastefully browned. How to use sauteéd vegetablesSautéed vegetables work well if you're already making a meal on the stove-top. Tacos, grain bowls, and egg skillets are all great ways to use sautéed vegetables. Example uses sauteéd vegetables:Pan Fried Turnips PicklingThis isn't necessarily a 'cooking method' but the fermentation nerd side of me can't overlook the ease and fun of quick pickling vegetables. There is no canning required, just some vinegar, salt, sugar, and spices if you wish. There are many different variations on pickling, which can be found along with instructions here. How to use quick picklesQuick pickles are great on sandwiches, as a topping for salads/grain bowls, or as a simple snack. Many different vegetables work well as quick pickles- just play around and find what you like! Example uses pickled vegetables:Hummus Sandwich with Pickled Carrots

The post 5 Ways to Cook Vegetables appeared first on Naturally..

0 Comments

You are used to seeing ants scurrying around your patio or driveway, ant hills protruding out of your grass, and even ants who've made their way into your home marching in a trail toward your pantry in warm months. Seeing ants in your home in New England in the winter could signal a serious problem, though. What Happens to Ants in WinterIn the winter months, most ants go into hibernation mode. Their body temperatures drop and they become sluggish. They prepare their colony for winter, sealing up their ant holes and burrowing into the warmer ground or behind tree bark. How Ants Survive the WinterUnlike humans, ants can go for a long time without food. They eat a lot of food in the fall to fatten up and prepare for winter. They huddle in groups to stay warm and protect the queen in a dormant state. What It Means if You See Ants in the WinterIf you see ants outdoors in the winter, it's likely there's been a warm spell that tricked them into coming out to seek food. Once the temperatures drop again, they will go back into hibernation. If you are seeing ants inside your home in the winter, it likely means that they've formed a colony inside somewhere. While they won't come indoors from outside in the winter, they will certainly remain active if they are already there. Why You Should Call in the ProfessionalsWhile ants in your home at any time of the year becomes a nuisance that you don't want to deal with, ants in your home in the winter is a much bigger problem. Having an ant colony infest your walls, attic, basement, or even pantry, can be damaging to your family and home. At a minimum, ants can invade your pantry and spoil your food. At worst, some ants, like carpenter ants, can actually cause structural damage. Our professional technicians are experts in dealing with ants in New England homes. We will work with you on exclusion techniques to eradicate the colony and rid your home of these pesky ants. Call us as soon as possible if you suspect a winter ant infestation! The post The Easiest DIY Desk Ever appeared first on Kaleidoscope Living.

The post The Easiest DIY Desk Ever appeared first on Kaleidoscope Living. This article is from PocketSmith, one of my partners. If you choose to sign up for the service from this post, I'll receive a small commission. If you're trying to get on the right financial track, you can make a small change and save money in the long run.

Setting big financial goals, like getting out of debt or saving for a home, can be daunting. But what if you usher in 2019 by focusing on one small change that could result in big gains financially? Start by picking one thing you'd like to spend less on. Then, take a moment to be curious about the reasons for the desire to change your spending habit. Do you think your curiosity will help you be more successful in making your one small change? Rather than if it was a New Year's resolution? The answer to the latter is yes, and we'll explain why below. In the meantime, here are some examples of small changes that yield big differences and help you save money over a year:

What does curiosity have to do with change?While change can be hard, curiosity – according to top mindfulness researcher Dr. Judson Brewer – feels good. So to effectively change a habit, you should enjoy the process by being curious about why this habit exists. In his TED talk, Dr. Brewer suggests that you first observe yourself acting on the impulse to do the thing you want to change, then get curious! Ask yourself:

Editor note: Miranda here. I love this. It's similar to finding your “why” when it comes to spending. Anytime you want to save money, spend better, and use your financial resources to improve your life, starting by answering these questions can help. How can we apply mindfulness to changing financial habits and saving money?If you've identified an area in which you believe you're overspending, you're already most of the way there because you don't need to justify the need for change. Take late fees as an example. Step back and be curious about why your habitual routines cause payments to be late, and penalties to occur. From there, take achievable steps to fix that one habit – perhaps by scheduling their payments when they arrive. And there's your small change. Conventional wisdom tells us that if we want to achieve a goal we must try harder and work harder, but perhaps we can make those New Year's resolutions stick by trying softer! Let's get startedTrack your spending and monitor progress on your small change with PocketSmith, one of the sharpest money management tools on the Internet. The team at PocketSmith would love to help you get there, so if you sign up for an account and Tweet or Facebook your small change to them, you could stand to win an upgrade to a one-year Super subscription worth $169.95. For example: Hey @pocketsmith! My #SmallChangeBigGains will be buying fewer coffees each week, therefore saving $700 in 2019. PocketSmith will pick ten of the best entries on January 9 (2019) and announce the winners on Facebook and Twitter, so get creative and share your tips! Remember to sign up, and use the #SmallChangeBigGains hashtag to qualify. As a bonus, if you sign up for PocketSmith from here, you will get half price on the first two months of PocketSmith Premium. Plus you'll receive an email guide designed to help you track and make your #SmallChangeBigGains Use this coupon to get 50% off the first two months of PocketSmith Premium: 50OFFPREMIUM-F4RG To redeem this offer go to PocketSmith, set up a free account and apply the coupon in the app via Settings>Subscriptions and Upgrades>Enter coupon. Then enter your payment details, and you are set to go.

Can One Small Change Save You Money in 2019? appeared first on Planting Money Seeds. Sponsored by Pederson's Farms Hey there! Neil Dudley, VP of Pederson's Farms, here. I'm so happy that you're joining us for the #JanuaryWhole30. I wanted to pop in and let you know about three ways our team at Pederson's Farms wants to help you stay prepped and eating well through your Whole30. 1 | We're Passionate about PorkWhether you're currently doing the #JanuaryWhole30 or planning to start one soon, we've created more than 20 Whole30 Approved® pork products to support you. Pederson's products are easy to find … they have the Whole30 Approved logo right on the label and are available online and in stores everywhere. I don't mean to brag, but we produce some really awesome, responsibly-raised, high-quality pork. Our pork tastes delicious and is raised without the use of antibiotics or growth stimulants, and never fed any animal by-products. Our products are minimally processed with no artificial ingredients, preservatives, nitrates/nitrites, gluten, lactose, or MSG … and wait for it … no sugar! As in “no sugar bacon?” You bet. We're famous for it. 2 | Our Whole30 Meal Prep Box Makes Meal Planning EasyI know the idea of Whole30 meal planning can be a bit daunting at first. Preparing to prep and cook nearly all of your meals at home means you need to find compliant recipes and compliant proteins to keep you going all month long. That's why we offer our Ultimate Whole30 Meal Prep Box. This Box was designed give you peace of mind when it comes to finding compliant, high-quality protein. It stocks your freezer with 10 of our most popular Whole30 Approved pork products in one easy order. The pricing works out to about $3.50 per meal … it's hard to beat that deal! Plus, when you purchase a bundle, we'll donate $10.00 towards our ongoing effort to support children with Type 1 Diabetes. 3 | We like tasty Whole30 recipes just as much as you doIn fact, we've created a 7-day Whole30 Meal Prep Guide stuffed with delicious Whole30 recipes. We'll share that for free when you order a Whole30 Meal Prep Bundle. It's full of delicious, satisfying, easy recipes inspired by the phenomenal Whole30 community. Want proof? I'm sharing 3 of my favorites in this blog post … just scroll down! But first … enter to win a free Whole30 Meal Prep Bundle HERE & we'll give you coupon for $15.00 off BLT Ranch Salad

Ingredients 1 pound Pederson's No Sugar Bacon Instructions PREHEAT oven to 400-degrees. Italian Sausage Egg Pizza

(Save or bookmark it here!) Ingredients 1 package of Pederson's Italian Sausage Instructions DICE your peppers and onion into 1/8-inch pieces, then set aside. Deli Ham Sushi Style Bites

Ingredients 8 slices of Pederson's Farms Black Forest Ham Instructions LAY a piece of deli meat on work service. Let them Eat Bacon (and Ham, and Sausage…)There you have it! The Ultimate Whole30 Meal Prep Box from Pederson's Farms is the perfect solution to finding tasty proteins that will make your Whole30 recipes shine. I wish you all of the best with your #JanuaryWhole30. Grab your $15 coupon HERE. This post was sponsored by Pederson's Farms. Thank you for supporting our Whole30 partners! The post Prepping and Preparing: 3 Easy Whole30 Recipes From Pederson's Farms appeared first on The Whole30® Program. More like A+ frame! Whether it's a beachside retreat or a cabin in the woods, the A-frame is a special type of building. You might recall the quirky triangle structures from vacations of yore, complete with avocado kitchens and shag carpets. But thanks to Instagram, nostalgia, and the allure of a certain way of life, the A-frame is back and better than ever. We've seen more A-frames as vacation rentals, tiny A-frame cabins that cost just $700 to build, and even a flatpack version that sets up in six hours. The latest to catch our eye are kit homes from Estonia-based Avrame. Indrek Kuldkepp, founder and owner of Avrame, first designed his own A-frame as a comfortable, efficient, and affordable home that could be built quickly and easily. After Kuldkepp realized that his A-frame cost about half as much as other homes to build, he decided to start a business selling self-build A-frame kits. Avrame now sells 11 different models of A-frames, from tiny backyard sheds to larger versions that can comfortably fit a family. All the models feature full-length windows to provide natural light The Duo 100, for example, is on the smaller size at about 613 square feet, with one bedroom and one bathroom on the main level and a sleeping loft up above. The largest model, the Trio 120, has 1,300 square feet of living space with three bedrooms and two bathrooms. When you buy an Avrame, the kit includes timber, the roof, the floor structure, windows and doors, building accessories, and a full set of drawings for building the structure. Avrame doesn't provide the building foundation or the interior finishings, but they do say that two people with reasonable skills can build the kits themselves. The entire process-from choosing a kit to moving in-usually takes four to eight months. Avrame says their homes are more efficient and maintain heat better than traditional A-frames thanks to durable structural insulated panels. You can also add onto to any model by making the A-frame longer. Prices range according to the size of the A-frame, with the largest model-the Trio 120-costing about $35,000. Since we first reported on Avrame, a US outpost has set up shop in Salt Lake City, Utah, with a new US-specific website here. Designed to pass the most common building code requirements in the U.S., Avrame USA works with each client to determine local requirements and makes adjustments as needed. The good news, however, is that this means that Avrame kits are now available in all 50 states. Head over here for more. /cdn.vox-cdn.com/uploads/chorus_asset/file/10328653/DUO_Interior_v_1.jpg) Courtesy of Avrame /cdn.vox-cdn.com/uploads/chorus_asset/file/10328659/DUO_Interior_v_4.jpg) Courtesy of Avrame /cdn.vox-cdn.com/uploads/chorus_asset/file/10328663/DUO_Interior_v_5.jpg) Courtesy of Avrame /cdn.vox-cdn.com/uploads/chorus_asset/file/10325137/TRIO_exterior_v_5.jpg) Courtesy of Avrame /cdn.vox-cdn.com/uploads/chorus_asset/file/10328635/TRIO_interior_v1.jpg) Courtesy of Avrame /cdn.vox-cdn.com/uploads/chorus_asset/file/10328641/TRIO_interior_v2.jpg) Courtesy of Avrame How Much Does Landscape Design Cost In Portland Sample Landscape Design Updated 12/18 to reflect the current cost of landscape design. When you hire a landscape designer you are paying them to develop a plan for your property. This usually involves drawings that show your landscape from above. You can see placement and relative sizes of proposed elements. Plants are placed, lighting fixtures are specified- the irrigation system layout may even be involved. This design, once in hand, can be given to licensed landscape contractors to bid and install. But what does it actually cost to get a landscape design completed? In general, a full landscape design will cost $500 - $5000. (Ross NW Watergardens usually charges between $1500 and $3000.) Some landscape designers charge an initial consultation fee, ranging from $100 - $250. (We have no initial consultation fee.) What factors affect price?  Modern Landscape Design by Ben Bowen of Ross NW Watergardens

There are obviously a lot of factors that effect what you pay for a landscape design. But, with the knowledge above you at least have an idea of what your design project could cost. The only way to find out for sure is to contact a local landscape designer and ask! Image:  We'll warn you now: these kitchen floor tile ideas aren't for the faint of heart. Tile isn't something you can easily change out, and making a bold commitment isn't for everyone. If you want to create a unique, eye-catching look in your kitchen, though, tile will make a major statement. Here are 3 ways to go bold with kitchen floor tiles, with real-life examples.Go BigBig tile? Big impact. If you go in this direction, however, limit your color choices-- the size already makes a statement, so keep it to larger patterns and a maximum of two colors for a look that's bold without being overwhelming. If you aren't sure how much of an impact the flooring makes, check out these images-- one with the kitchen flooring in place, another with the floor edited out, so you can truly see how the tile changes the entire feel of the kitchen. Without the bold flooring, these kitchens don't stand out. It's the floor tile that sets them apart. Photo Credit: Theartofdoingstuff.com Choose small but powerfulThe opposite is true for smaller tiles-- you can go with two or more colors, or choose more intricate kitchen floor tile patterns. Photo Credit: CountryLiving.com Get a real feel for the impact of small but mighty floor tile by comparing these images: Take inspiration from natureThe natural grooves and wave patterns in natural stone creates a unique texture that can soften the look of your kitchen while still giving it a unique vibe. Photo Credit: futuristarchitecture.com See the difference in the feeling of the space by comparing these images: Photo Credit: futuristarchitecture.com

Every detail in a kitchen combines to create the overall impact, but when choosing standout features, many homeowners often overlook the floor. So if you want to go bold, beautiful and unique, explore your flooring options. Do you have a unique kitchen floor tile pattern? Share it with us over on Facebook! Category:

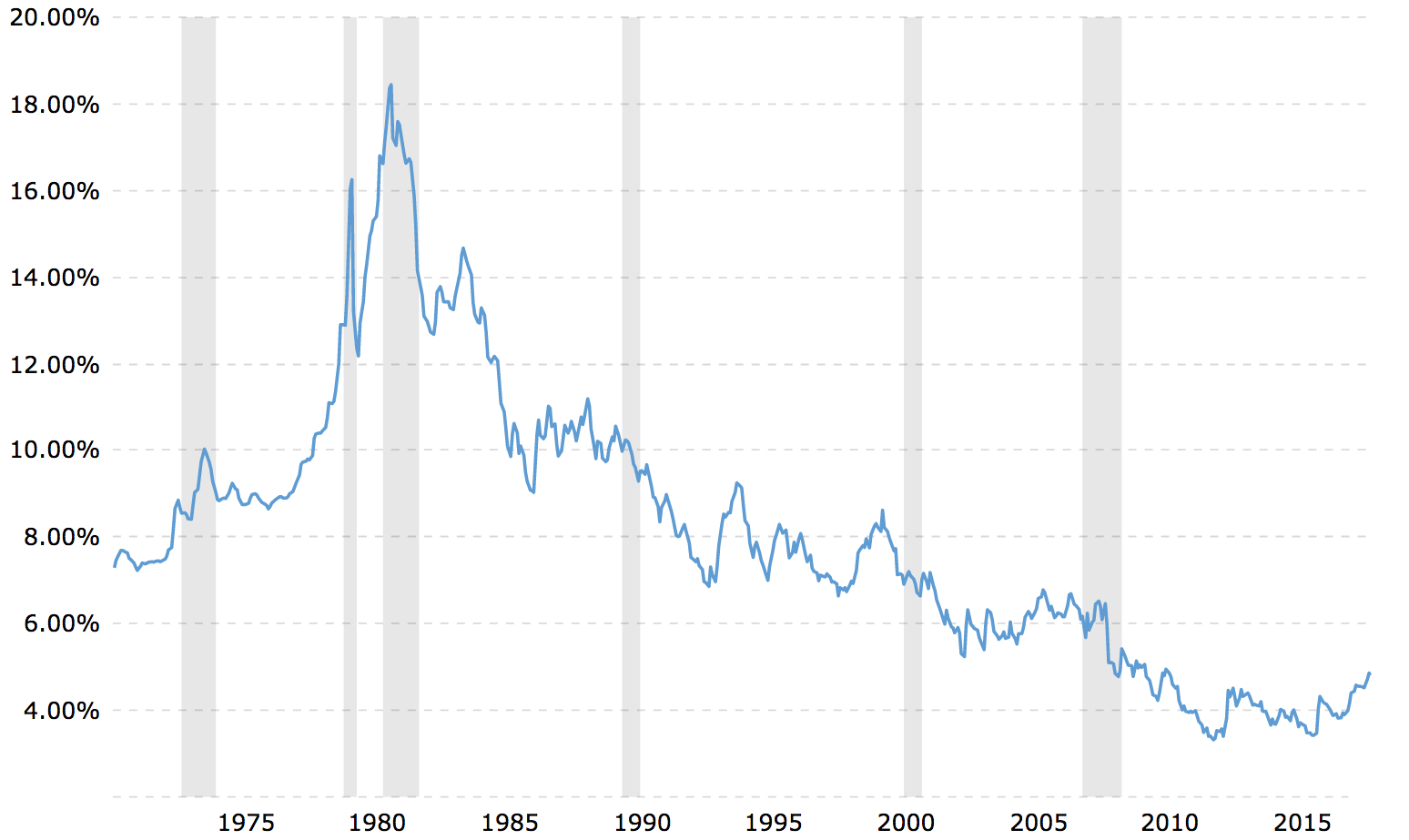

Instead, I got something better. It was letter from my bank saying my adjustable rate mortgage interest rate is going up! This is the first time I've ever received such a letter because, in the past, I would always refinance my 5-year ARM (my preferred ARM term) lower before the fixed period was up. But with interest rates having moved up since I bought my house in 2014, the logical thing to do was keep holding it until the reset. The Origins Of Our 5-Year ARMWe bought a San Francisco single family fixer in 1H2014 for $1,250,000. We were tired of living in the north end of San Francisco for the past 9.5 years and wanted a change of scenery. Originally, we had planned to relocate to Hawaii, but when we found our current house with ocean views, we though this would be a good compromise. We put down 20% and took out a $992,000 5-year ARM. Originally, I was going to put down 32%, because I had about $430,000 come due from a 4.1% 5-year CD. But with a mortgage rate of only 2.5%, I felt it was worth borrowing more and investing the difference. The 2.5% mortgage rate was based on the one year LIBOR rate + a 2.25% margin – 0.25% discount for being an excellent customer. Back in 2014, the one year LIBOR rate was at only 0.5%, hence my 2.5% rate. The London Interbank Offered Rate (LIBOR) is the average interest rate at which leading banks borrow funds from other banks in the London market. LIBOR is the most widely used global “benchmark” or reference rate for short-term interest rates. Check out the historical one-year LIBOR chart below.

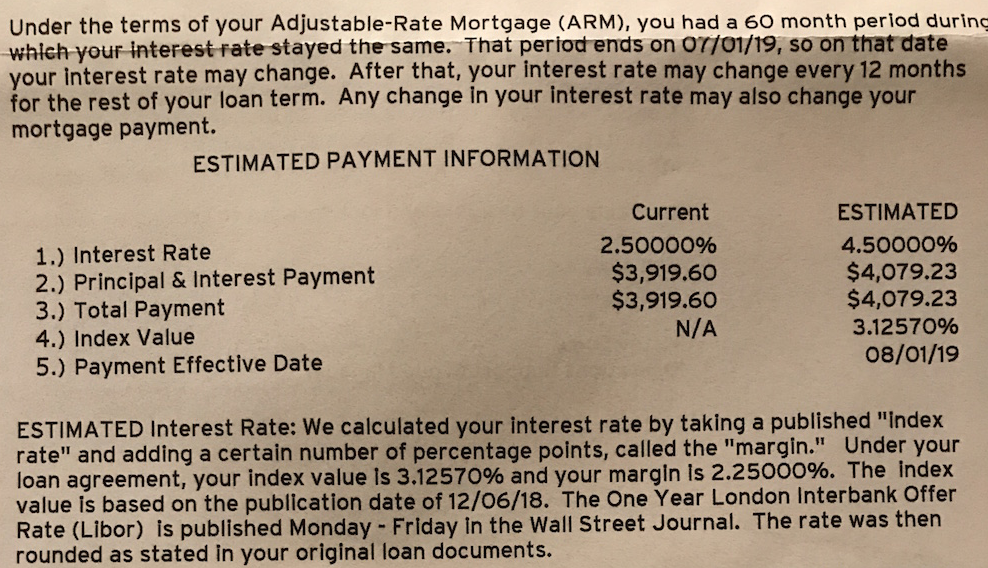

As you can tell from the one-year LIBOR chart, I bottom-ticked my mortgage rate in 2014. Some of you might be thinking that instead of getting a 5/1 ARM, I should have gotten a 30-year fixed rate instead. But given my strong belief that we will be in a permanently low interest rate environment for the rest of our lives, I felt that paying 0.85% – 1.25% more for a 30-year fixed rate was a waste of money. So my actions followed my brain. Besides, the average homeownership duration in America is only around 8.7 years. At most, one may consider taking out a 10/1 ARM to match durations. As I planned to either sell my home within 10 years in order to buy a nicer home in Hawaii or pay off the mortgage during this time frame, to me, taking out a 5/1 ARM was worth the “risk.” Regardless of whether you want to waste your money on a 30-year fixed mortgage or not, mortgage rates have indeed gone up for all of us since 2014. Based on the current one year LIBOR rate of ~3.1% + my margin of 2.25% – my 0.25% for being an excellent client, my new mortgage rate should be a reasonable 5.1% when it resets in mid-2019. If I end up paying 5.1% for the next five years, my average mortgage rate over a 10 year period would be 5.1% + 2.5% = 7.6% /2 = 3.8%. 3.8% is pretty much in-line with the rate I would have gotten if I just locked in a 30-year fixed rate mortgage in 2014. However, with the money saved from not paying a 30-year fixed mortgage and the $100,000+ less in downpayment, I ended up investing the difference and earned a ~7% return on average from 2014 – 2018 because the stock market went up until 2018. Although I did eek out a 0.8% gain in 2018. But surprise! I won't be paying an estimated 5.1% mortgage rate in 2019. Instead, my letter says that I'll be paying an estimated 4.5%. Have a look at the portion of the letter below.

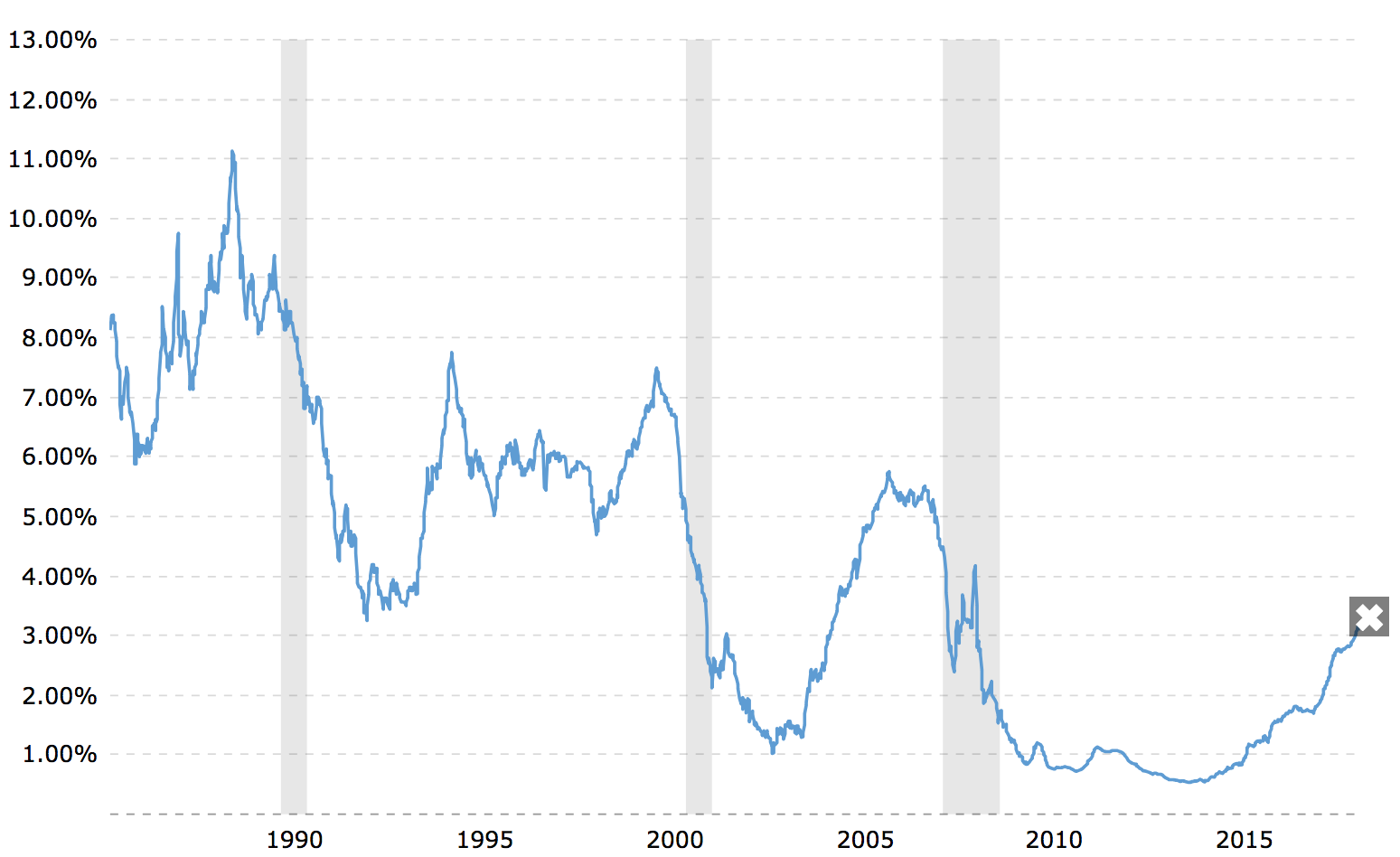

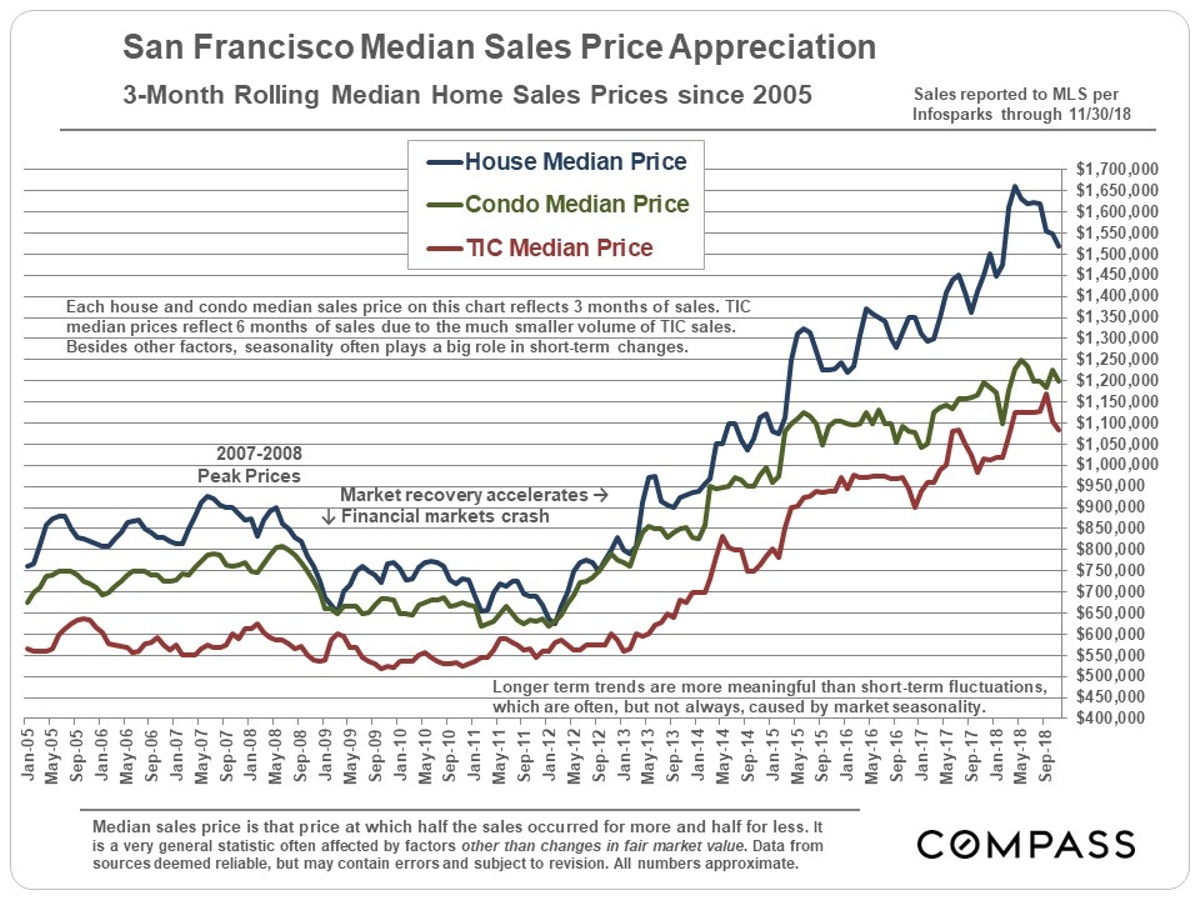

The letter clearly states how they calculate my mortgage rate, yet for some reason, they still come up with an estimated rate of 4.5% instead of 5.1%. Perhaps my good customer discount of -0.25% will grow to -0.85% next year? Or perhaps my bank simply made a mistake in their calculation. No, no. Banks aren't stupid. The reason why my rate only goes up from 2.5% to 4.5% is that under the terms of my mortgage, my ARM can only reset by at most 2% after the initial 5-year fixed rate of 2.5% is up. This maximum reset amount is pretty standard among ARM loans. But this reset amount is something you must have your bank point out in the document. The other thing to note is that ARM loans generally have a maximum mortgage interest rate they can charge for the life of your loan. In my case, that maximum is 7.5%, but we're never going to get there in my opinion. Unfortunately, after one full year at 4.5%, my bank can raise my ARM by another 2%, bringing my mortgage rate up to 6.5% for year seven. However, I doubt rates will keep on surging higher as the global economy slows. Instead, by the time my ARM reset occurs again in 7/1/2020, we might very well be in a recession with one year LIBOR rates moving back down. Paying Down PrincipalIn order to make more money, mortgage brokers and banks LOVE to scare the heck out of inexperienced homebuyers by saying their payments will surge higher once an ARM resets. They don't show them a 35-year historical chart of declining interest rates. By scaring their customers, they have a higher chance of locking them into 30-year fixed rate mortgages for fatter margins. Don't be fooled.  Historical 30-year Mortgage Interest Rate Chart You can see from the letter that despite my mortgage rate increasing from 2.5% to 4.5%, an 80% increase, my monthly payment is only expected to increase from $3,919.60 to $4,079.33, a mere 4% rise. The reason for the slight increase in monthly mortgage payment is because we've paid down 32% of our loan in 4.5 years ($992,000 down to $734,000). Paying down over $250,000 in our mortgage was partly due to normal monthly principal payments coupled with random extra principal pay downs. Although the 2.5% interest rate is low, paying down mortgage debt has always been part of my long term investment strategy. Following my FS-DAIR strategy, I would regularly try and use 25% of my free cash flow to pay down debt and use the other 75% to invest. Again, I'm just taking action based on my own advice. I kept on paying down principal randomly until the 10-year yield breached 2.5% in December 2017. Once the 10-year yield was higher than 2.5%, I stopped because I was now getting an interest-free mortgage since I could simply invest the amount of my mortgage in a 10-year bond yield to cover all my payments. Living for free is one of the best things ever! If I had taken out a 30-year fixed mortgage for 3.625%, I wouldn't have been able to experience interest-free living. Your mileage will vary in terms of how much principal you actually paid down during the initial fixed rate period of your ARM. However, even if you didn't pay down any extra principal during a five year period, you will have still paid down ~10% of your principal balance, depending on your interest rate. An Appreciation In Your Home's ValueEven if you've got to pay a higher mortgage rate when your ARM resets, you may be pleased to discover that your home has appreciated in value during the fixed rate period. The San Francisco median home price increased from $1,100,000 in 2014 to ~$1,500,000 today, or a 37% increase. A $420,000 principal increase more than makes up for a measly $159.63 monthly increase in mortgage payment, roughly half of which is going to pay down principal anyway.

Again, your home's appreciation amount will vary. Unless you timed your home purchase completely wrong, such as buying in 4Q2006 – 4Q2008 or maybe 1Q2018 (jury is still out), you'll likely come out OK. Even if you did purchase at the most recent peak, normal downturns usually last no more than 3-5 years with 10% – 20% corrections. Make A Mortgage Pay Down PlanGiven I have until 7/1/2019 before my mortgage rate jumps from 2.5% to 4.5%, I plan to keep paying my mortgage as usual and not pay anything extra to principal. As soon as I exhaust all 60 months at 2.5%, I will pay down $50,000 in principal on month 61. After the initial $50,000 extra principal payment, I will keep paying down between $20,000 – $30,000 a month in extra principal until the mortgage is gone or until I find my Hawaiian dream home. Based on my extra principal payments, the mortgage should be completely paid off by January 2022, or about 7.5 years after I first took out the loan. Anything can happen between now and January 2022, which is why it's prudent to continue investing and paying down debt while having a good cash hoard. You can now earn a healthy 2.45% in a money market account with CIT Bank, for example. That's huge, since just several years ago, savings rates were under 0.5%. Earning a 4.5% rate of return is excellent at this stage in the economic cycle, but so is having enough cash to find a gem of a property in Hawaii at a big discount. And boy, am I seeing discounts everywhere now! The alternative solution to aggressively paying down principal is to simply refinance my mortgage when it's time to reset to another 5/1 ARM. After checking online for the latest mortgage rates, I can get a 5/1 ARM jumbo for only 3.25%. This means that after 10 years, my blended interest rate is 2.875%. Not bad at all. Article Summary 1) Match the duration of your mortgage's fixed duration with the estimated ownership duration or the length of time you estimate it will take to pay off the mortgage. 2) Paying for a 30-year fixed rate mortgage might provide you more peace of mind, but you're likely overpaying for that peace of mind. 3) Read the terms of your ARM loan carefully and figure out what is the maximum interest rate increase during the first reset and what is the lifetime interest rate cap. 4) Try to make extra payments during your ARM's fixed rate period to relieve potential interest rate pressure during the reset. 5) Don't borrow more than you can comfortably afford = no greater than a 80% loan-to-value ratio with a 10% cash buffer after a 20% downpayment. Being overly leveraged is what consistently destroys people's finances. Readers, why do people take out overpriced 30-year fixed rate mortgages when the average homeownership duration is less than 9 years? Why pay a higher rate when interest rates have gone down for 35+ years in a row? The post The Anatomy Of An Adjustable Rate Mortgage Increase appeared first on Financial Samurai. 'House Party' Podcast: Is 'The Bachelor' Mansion Decor Hideous? Plus, What Not to Do in the Bedroom1/12/2019  Getty Images; realtor.com “House Party” is realtor.com's official podcast about the overlapping worlds of real estate and pop culture. Click the player above to hear our takes on this week's hot topics. It's January, so that means three things are for certain: Gyms everywhere are packed with sweaty resolution-makers, the days are slowly-but finally-getting longer, and, of course, there's an all-new season of “The Bachelor.” In the premiere this week, we were introduced to the 29 women-and one sloth-who are vying for the heart of Colton Underwood, the franchise's first-ever virgin bachelor. We have thoughts (like the fact that it was three hours of our lives we'll never get back), but since this isn't a “Bachelor” podcast, we'll refrain from going too far down the rabbit hole. We did, however, go all-in on “The Bachelor” mansion decor, which changes from season to season. Is it haute or hideous? Then Erik, Natalie, and Rachel discuss whether they're officially Marie Kondo-verts after watching three episodes of the pro organizer's new Netflix show, “Tidying Up.” There's a lot to unpack here (clutter pun!). Speaking of cleaning, a man in California was caught on camera this week licking a doorbell clean. For three hours. That's 180 minutes of licking, folks. Why? Well, we're sure he had his reasons-and we're pretty sure those reasons included bath salts. But isn't it fun what our home security cameras can capture these things? (P.S. The licker is still at large. Slurp!) Next, we take things into the bedroom. (Not like that, you sickos.) Rachel admits to having a few items in her boudoir that could be keeping her up at night, and we're pretty sure the rest of you do, too. How is your bedroom subconsciously stressing you out? You'll have to listen to find out! We also discuss some of the biggest little bungalows for sale right now. They are cute and spacious, and we seriously want them all. And, of course, we've got celebrity winners and losers (or, as Erik prefers to call them, “famous people who just didn't do so great in real estate this particular week but they're probably very nice people, actually.”) Our winner made real estate moves (like Jagger), and our loser had to shred the price of his San Francisco mansion. So what are you waiting for? Listen already! Subscribe on Apple Podcasts, Google Play Music, Spotify, or wherever you get your podcasts. And, by all means, throw us a five-star rating if you like what you hear. The more good ratings and reviews we have, the easier it'll be for people to find us. Have a wacky home-related story you're dying to share? Wish you could finally get your real estate questions answered? We're all ears. Reach us at [email protected], or tweet us @housepartypod on Twitter. Stories we discussed on 'House Party' this week:6 Shockers About 'The Bachelor' Mansion We'll Bet You Never Knew Can Marie Kondo Help You Organize in 2019? Find Out Here Watch Marie Kondo Battle the 'Biggest' Mess She's Ever Seen De-Stress Your Nest: 7 Things in Your Bedroom Making You Anxious A Bungalow Doesn't Have to Be Small! 9 Jumbo Bungalows for Sale Metallica's Kirk Hammett Shreds $1.1M Off Price of San Francisco Mansion Ben Affleck and Jennifer Garner Finally Sell Their Home to a Buyer You Won't Believe Adam Levine Reportedly Buys Beverly Hills Estate for $35.5M The post 'House Party' Podcast: Is 'The Bachelor' Mansion Decor Hideous? Plus, What Not to Do in the Bedroom appeared first on Real Estate News & Insights | realtor.com®. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

January 2019

Categories |

If you need a desk that won't take up a ton of room that it is affordable and easy to make, this DIY desk tutorial is for you! The floating desk design takes up very little floor space and it's easy enough for even inexperienced DIYers to tackle. Happy new year, friends! I hope 2019 ...

If you need a desk that won't take up a ton of room that it is affordable and easy to make, this DIY desk tutorial is for you! The floating desk design takes up very little floor space and it's easy enough for even inexperienced DIYers to tackle. Happy new year, friends! I hope 2019 ...

I'm so excited to share with you something I got in the mail the other day. No, it wasn't a notification that Financial Samurai had won an award for being the best personal finance site. My site is too focused on understanding hard things to make us all rich to appeal to the masses.

I'm so excited to share with you something I got in the mail the other day. No, it wasn't a notification that Financial Samurai had won an award for being the best personal finance site. My site is too focused on understanding hard things to make us all rich to appeal to the masses.

RSS Feed

RSS Feed